{kind=link}

I have said for a year or two, maybe longer, that recapture was the next big thing in mortgage loan.

Instead of going out and spending a lot of time and money on acquiring new customers, why not just take advantage of those you already have?

This is especially true when it is no longer easy to strain with a home loan thanks to much higher mortgage rates.

Mortgage companies realized this and began to service their own loans so that they could transform existing customers into repeated customers.

And that is clear what Rocket is doing by acquiring the nation’s biggest loan visit, Mr. Cooper.

Rocket wants to take advantage of Mr. Cooper’s Giant Stall of existing homeowners

In short, Rocket Mr. Cooper to take advantage of millions of recovering options.

To give you an idea of how important recovery is too rocket, the word is used seven times in their press release.

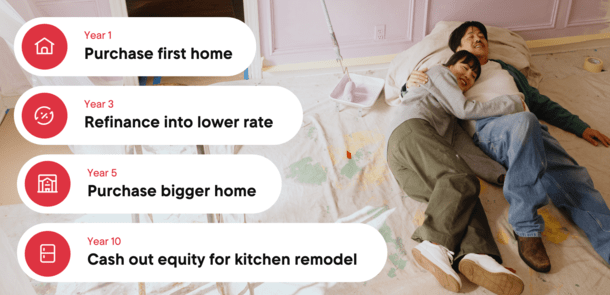

For the uninitiated, recovering means to stem another loan for an existing customer you have earned in the past.

An example would be someone who used Mr. Cooper to get a home purchase loan that later uses Mr. Cooper to complete a rate and refinancing to obtain a lower priority rate.

With this link, Rocket would be the one who benefits from any subsequent loans offered to Mr. Cooper customers.

And there are many of them, considering that Mr. Cooper is the largest loan service in the country.

At the last look, Mr. Cooper approx. 6.7 million loans that service customers, all of whom are homeowners who can beat another product.

It may be an interest rate and term refinancing if/when mortgage rates fall, or another priority loan, such as a home capita loan if the rates do not come down.

Maybe it’s a subsequent home purchase loan after selling and moving up to another property.

There are plenty of scenarios to take, and instead of going out and looking for homeowners with high inhabitants (or home buyers), Rocket can simply scan its own database.

And thanks to new technology, it is easy to determine who might want/need to get another loan.

Robet will be your mortgage loan for life

What makes this merger such a valuable proposal for rocket is the fact that they are already a leader in the recoverable.

In short, they know how to sell. Especially if they already have someone in their funnel.

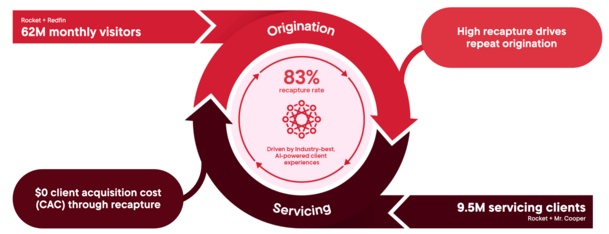

It explains their second major purchase of Redphin and its 50 million monthly visitors.

While they have failed to catch a large part of the Home Purchase Loan market (this honor goes to United Wholesale Mortgage), they are the leading lender for mortgages in the country.

Also with a wide margin. They patterned about the double of the refinancing volume of UWM in 2023 (the past year available), nearly $ 29 billion against $ 14.5 billion per year. HMDA data.

And they managed it in a year when mortgage rates hovered in the area 6% to 7.5%.

So it is clear that they are very good at selling to existing homeowners looking for the relief of interest rates or a paid refinancing.

With mortgage rates raised over the past few years, there are now millions on millions of homeowners with loans starting with a 6 or a 7.

If and when interest rates lighten, you should think that Rocket will be the first to offer them a new loan.

They have already made a case for what spell billions in loans from Mr. Cooper that is in the money for a refinancing.

About $ 41 billion can be refinanced if the 30-year-old fasting is 6.5%, and $ 100 billion if this rate comes down to 6%. If they can deliver a higher recovery rate, the upside is even greater.

For the record, it simply offers Mr. Cooper clients a 50-base point (0.50%) or better advantage over their current priority rate.

And the glaze on the cake is that there is a $ 0 client collection cost (CAC) via re -capture.

Rocket is already leading the industry in re -capture and this will only make them better at selling

We know that Rocket is good at selling and we know they are excellent at regaining existing clients.

The only other piece is labor and financing. And they have it too.

Rocket has about 3,000 mortgage loan managers ready to take loan applications and start transferring Mr. Cooper customers for Rocket mortgage customers.

And it’s driven by AI, including 1.2 million monthly calls log prints to analyze what works and what doesn’t.

Not to mention 30 Petabytes data and get “understanding almost 7 million additional clients and 150 million annual customer interactions.”

In other words, Rocket will be even better at selling And operates the company’s detention of 83%, which has already tripled the average of the industry, even higher.

This can make the next one impossible for external lenders to compete, provided they even get the chance.

With the technology in place, Rocket will probably be first for the customer in most scenarios, so the only hope for external companies will be if the customer takes the time to shop around.

This is something I always recommend, especially with the re -capture of the great focus now.

In short, if a lender reaches out, reach out to other lenders.

If you don’t get more offers, you never know what else is out there. And studies prove that even a further rate offering can save you thousands.

On top of these synergies, Rocket plans to optimize earnings on Escrow deposits and make money on recurring service fees.

So not only they get a lot of new loan prospects, but also a robust service company to start.

Rocket Mr. Cooper Deal is expected to close in the fourth quarter of 2025

The All-Stock transaction is already unanimously approved by both boards of rocket companies and Mr. Cooper.

And is currently expected to close in the fourth quarter of 2025.

As part of the agreement, Mr. Cooper shareholders receive 11 shares of Rocket (sneezing: RKT) for each share of Mr. Cooper Common Stock.

Mr. Cooper Stock (Nasdaq: Coop) rose approx. 17% on the news for just over $ 122 per Stock.

The expected acquisition costs of $ 9.4 billion would appreciate Mr. Cooper shares $ 143.33 based on the closure course on March 28, 2025.

It represents a 35% premium compared to the volume -weighted average price (VWAP) of Mr. Cooper’s joint stock in the last 30 days.

Mr. The Cooper shareholders will also receive a dividend of $ 2 per year. Share in connection with the implementation of the transaction.

As I said with the Redfin acquisition, it is clear that Rocket wants to be the No. 1 mortgage loan in America again after losing his head to UWM.

And with a total of $ 2.1 trillion and access to nearly 10 million clients (one of every six mortgage loans in America), they will certainly be difficult to beat.

Rocket refers to it as a “origin -service recovery of flywheels”, which brings new customers into their ecosystem via Redphin and seems to preserve them as customers for life through loan service and recovery.

(Photo: Mike W.)

Before creating this site, I worked as a banking director of a wholesale loan in Los Angeles. My practical experience in the early 2000s inspired me to start writing about mortgage loans 19 years ago to help potential (and existing) home buyers better navigate the home loan process. Follow me on x for hot take.